Work-from-home will shift power from workers to owners

And examining the role of capital, investors, and founders in shaping the future of technology

Today I’m going to try to tie together a few concepts to try and understand the sudden shift to remote work in tech, while continuing my series on how my worldview has shifted since becoming a socialist. At the end I try and develop an understanding of how capitalists influence the kind of technology that gets developed, not always to the users’ benefit. And by the way, thanks to the Twink Revolution podcast for having me on this week to bullshit about tech and DSA.

There are a lot of silver linings to the collapse of the Bay Area as the all-but-sole tech hub of the world: spreading the wealth of tech around geographically, flexibility for workers to live where they want, and relieving pressure on Bay Area infrastructure. I frequently deride the Sand Hill tariff, the idea that anytime any person on earth engages in commerce, orders a taxi, gets takeout, or messages their loved ones, a company in California and a venture capitalist on Sand Hill Road gets a cut. That had to change. In the past, when I was a bit more of a tech booster, I would have focused on these positive aspects and gotten excited about the possibilities of a more diverse set of people building towards our glorious technological future.

Today, I’m more likely to ask who benefits? and who loses? when I see a change in the workplace. Or, to quote my favorite Game of Thrones character: “What's the worst reason they could possibly have for saying what they say and doing what they do? Then I ask myself, 'How well does that reason explain what they say and what they do?’” (I confess that Game of Thrones for me is like Harry Potter for liberals—it’s where all my political understanding comes from.)

{kind=link}

So here’s my particularly naive I-used-to-believe for the week:

I used to believe everyone working in tech was on the same side, really. We are all engaged in a collective endeavor to build new ways of living in the world assisted by technology, leading to a better world and less toil. The people who invest in tech companies mostly love products and strive to foster creation, and they’re rewarded for doing so. Founders make sacrifices and take on risks to organize bastions of order in a sea of chaos in order to advance technology. Users are equal stakeholders in the process, as ultimately everything we do serves them, and they should be both invested in and grateful for the process of technological development.

After analyzing the structure of the tech industry more closely, now I believe that the tech industry, like any other industry, is made up of actors with irreconcilably contradictory interests. The investor tier of the industry only seeks profitable returns, which are often at odds with the interests of founders, workers, and customers. Investors, founders, and highly-paid workers generally occupy contradictory class locations.

In my defense, Stanford in the 2000s basically taught this to STEM students.

Winners and losers in WFH

Kim-Mai Cutler has a good summary of winners and losers from the WFH trend. I would add to the list of losers: my paycheck, assuming I ever work in tech again.

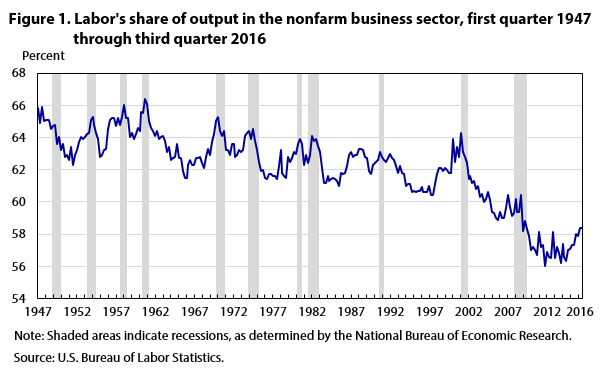

Let’s talk about labor’s share of income. This is, as I understand it, the sum of all wages earned divided by nominal GDP. Basically, it says what slice of the pie created by mixing labor and capital accrues to workers and what share is given to owners. Since the 1980s, labor’s share has been in decline; this is a symptom of that new kind of liberalism they keep talking about. Let’s try to understand the division of incomes between capital and labor using a class war hypothesis: the interests of owners and workers are fundamentally opposed, and a dollar that goes to the owner is a dollar that doesn’t go to the worker. This is in contrast to a growth hypothesis that would argue something like “a rising tide lifts all boats”. I can imagine that the growth hypothesis held true at some point in capitalist history. It does not seem remotely defensible in 2020.

{kind=link}

I argue that even as they ‘flatten’ the distribution of wages, WFH policies are going to result in a net gain for owners and a net loss for workers, considered as a class. An engineer that cost a company $400k (including benefits) in the Bay Area is going to cost them less now. The pool of workers has increased in size, so I should expect wages in the Bay Area to go down now. Once WFH is normalized, it will matter less if an engineer is in Cleveland or Warsaw, so now American tech workers are competing with engineers around the entire world. Operating expenditures at companies will fall accordingly, and associated expenses like real estate and office maintenance will go down as well. That’s more money for the company to spend on stock buybacks, and that’s what they will do.

Expanding the reserve army of labor

One astute reader asked, essentially, if a company now chooses to hire engineers “two for the price of one”, is that a net benefit to workers since two cheaper workers have been hired? That’s a good question that I’m still thinking through. Marx examines the point in Wage Labor and Capital when considering whether the interests of labor and capital are aligned, since a wealthier capitalist can hire more laborers: (shout-out to the Friday night Marx reading group for explaining this to me)

Capital can multiply itself only by exchanging itself for labour-power, by calling wage-labour into life. The labour-power of the wage-labourer can exchange itself for capital only by increasing capital, by strengthening that very power whose slave it is. Increase of capital, therefore, is increase of the proletariat, i.e., of the working class.

And so, the bourgeoisie and its economists maintain that the interest of the capitalist and of the labourer is the same. And in fact, so they are! The worker perishes if capital does not keep him busy. Capital perishes if it does not exploit labour-power, which, in order to exploit, it must buy. The more quickly the capital destined for production – the productive capital – increases, the more prosperous industry is, the more the bourgeoisie enriches itself, the better business gets, so many more workers does the capitalist need, so much the dearer does the worker sell himself. The fastest possible growth of productive capital is, therefore, the indispensable condition for a tolerable life to the labourer.

But what is growth of productive capital? Growth of the power of accumulated labour over living labour; growth of the rule of the bourgeoisie over the working class. When wage-labour produces the alien wealth dominating it, the power hostile to it, capital, there flow back to it its means of employment – i.e., its means of subsistence, under the condition that it again become a part of capital, that is become again the lever whereby capital is to be forced into an accelerated expansive movement.

I think this is easy enough to understand: under capitalist hegemony, what’s good for the boss is good for the worker, kind of, but it strengthens the power the boss continues to hold over the worker. This is the pinion of capital. Maybe the only strange concept might be “accumulated labour versus living labour”. This is a way to view capital: as dead labor. If I spend some time writing code for a company, the time is gone and the product of it has become capital owned by the company. The labor is dead as soon as I finish producing the output.

We should expect capital to make moves that lead to cheaper labor power in the future. Any businessperson will try and abstract over the providers of their inputs; having multiple sellers for an input detracts from their ability to extract monopoly rents. Socialists push this idea even further: unemployment is actually an essential trait of capitalism. There’s a concept introduced by Engels and expanded upon by Marx: the reserve army of labor:

Big industry constantly requires a reserve army of unemployed workers for times of overproduction. The main purpose of the bourgeois in relation to the worker is, of course, to have the commodity labour as cheaply as possible, which is only possible when the supply of this commodity is as large as possible in relation to the demand for it, i.e., when the overpopulation is the greatest.

These unemployed workers can be called up when needed for production. When they are not employed, they serve the use of giving capitalists an easy and powerful BATNA when negotiating with an employee: hire another unemployed, potentially desperate worker instead. The presence of unemployed workers reduces all our wages.

The economist Michał Kalecki took this even farther: the threat of unemployment and the reserve army of labor are essential tools for capitalists to discipline the workforce. Although “full employment” would increase the rate at which capital and labor-power are mixed into more capital, thus increasing returns on capital, full employment would also mean losing the disciplinary tools capital needs to effectively manage a workforce. He writes that full employment

would cause social and political changes which would give a new impetus to the opposition of the business leaders. The “sack” would cease to play its role as a disciplinary measure. The social position of the boss would be undermined, and the self-assurance and class-consciousness of the working class would grow. . . . “Discipline in the factories” and “political stability” are more appreciated than profits by business leaders. Their class instinct tells them that lasting full employment is unsound from their point of view, and that unemployment is an integral part of the “normal” capitalist system.

I don’t know if the concept of a class instinct is explored rigorously. I suspect a class instinct appears when we discuss a UBI, like Andrew Yang’s modest Freedom Dividend. Workers might imagine what $1,000/month would mean to their families, while bosses who pay $7.25/hour might wonder if their employees will stop taking shifts. The class instinct also captures something true to me: there is never a smoke-filled room where the cabal of capitalists decides the future of the world. Instead, it is always a system of filters and subtle nudges. To me, reasoning about a class having aspirations works on an aesthetic level, the way a paintbrush might want to make a particular stroke or a Python function might want to have a particular signature.

If there was ever an industry where capitalists felt the first pangs of losing ground to workers for their scarce skills, tech is it. If capital is smart, it will find ways to disempower workers, lest the nascent tech worker movement gain more ground. Disciplining brilliant but unruly software engineers, newly homebound, with a threat of outsourcing their jobs suddenly feels a lot more possible.

The reserve army of founders

If we look deeply into the tech industry, we realize it’s hard to put everyone into the category of capitalist or worker. Is the lowest level of manager really a capitalist even if their reports might make more money or be higher-level than them? Does an entry-level associate VC really have the same interests as a factory owner?

Erik Olin Wright proposes a resolution to these questions: “Highly educated professionals, managers, and many self-employed people, for example, occupy what I have called contradictory locations within class relations and have quite complex and often inconsistent interests with respect to capitalism.”

This contradictory class location shows up among highly-paid workers and managers, but there’s an argument to be made that even executives and investors have capital-aligning and capital-opposing interests. I argue that by manipulating these capital-aligned classes of people, capital is instinctually able to direct the development of technology towards ends that will lead to greater returns on capital.

Here’s a quick sketch of the tech ecosystem: Holders of capital have one goal: the highest-possible returns on that capital. These banks, pension funds, sovereign wealth funds, or family offices hand over their funds to venture capitalists who they expect to make high returns. These investors look around the technology industry and the market to evaluate what kinds of businesses they should fund. Then they hand over those funds to founders who run firms that hire workers with those funds. Ultimately the customers (ad buyers or purchasers of the firm’s products) pay into the firm, and the wealth trickles back up the chain to the holders of capital.

You can see that the banks and the investors have a lot of power here. Competition between founders for scarce investments means that founders are subject to discipline from investors in a way similar to how workers are disciplined by managers and owners. I don’t want to get into the notion that founders are “exploited”, as they are ultimately much more aligned with capital than with workers, but there is clearly something there.

What I’d rather talk about is how investors use this disciplinary power to steer technological development towards technologies that will end up giving recurring returns to capital. Today there is a ton of investment going into machine learning startups. The hope for a ML founder is that they create a machine learning technology company that is immensely valuable; that many customers want to pay them for their product, whether it’s a self-driving car or an algorithm hosted in the cloud. What does the investor hope for? That they’ve invested in not just one 1000x hit company, but in a whole sector that is going to win returns (you often see VC firms investing in companies competing within a space). With a technology like machine learning (or miniaturization, or developer tooling, or lots and lots of things), we see accelerating returns on the technology itself: the more we collectively do ML, the better we collectively get at ML. Machine learning is a technology with the potential to massively shift the balance of power from labor towards capital by automating away jobs and pushing more workers down towards precarity. As a class, investors have to be ecstatic about the potential of machine learning. Already threatening workers with offshoring, now capitalists increasingly threaten workers with ML-powered automation.

Another product area I think exhibits this capitalist class instinct is smart home technology. Over the years, we are seeing more and more cameras (and other sensors) appear in our houses. First on our computers and phones, now on our Portals and Echos and our workout smart mirrors. These devices have the potential to be major sources of data for machine learning systems to understand and target consumer behavior. And eroding the norms against being surveilled in the home will, in aggregate, give corporations access to more and more data over time.

Now, absolutely no product manager is saying “I want to monetize the data collected from this camera we sell to families to stay in touch.” No founder or investor is bragging that customers are inviting ad networks into their bedrooms, because that’s not what’s happening. But, as a class, is capital smart enough to understand that more cameras mean more data which will mean more returns a decade down the line? If so, its agents can choose to fund the AR headsets, smart mirrors, and video units that will put more sensors in more homes over time. If an investor wants more sensors in the home, they can hold out for founders that are willing to build firms around products that offer such sensors. And when the firm fails to find sufficient returns by selling a product to an end-user, the investor can discipline that founder and force them to monetize the data they’re collecting, or replace them with an executive that will. Down the line, the capitalists will find synergies between their investments in smart homes, behavior-tracking ML systems, and ad delivery networks.

This is getting handwavey and I’m not even 100% sure about class instincts, so I’ll leave it at that–the technology that gets built is the technology that will produce returns for capital, and capital (sometimes) takes the long view.

Some thoughts provoked by trying to avoid the conundrum of saying founders are "exploited":

I don't have a citation, but you can look at Marx's comments in Capital on how capitalism (as a system) disciplines the owners of firms, i.e. Capitalists. Founders—possessing an ownership stake which predominates their interests over and above any wage—are at best a fraction of the Capital class. Maybe what you mean is that their will is subjugated to social imperatives of the class? Would it help then to say that Bourgeoise freedom is (beyond legal rights of citizens and humans) principally the freedom of a wealthy consumer? Or perhaps the freedom of disproportionate power in society. In another sense, even capitalists are not free under capitalism. However, they lack the necessary class interests to be a historical force capable of changing that situation.

Another quick footnote: I suspect the most important contradictions of class position for tech workers are (a) created by payment in equity/stock, and (b) created by the potential to become founders thanks to venture capital. Maybe these dynamics or potentialities (rather than simply static class positions) might be useful for your analysis.